How to design your marketplace transaction flow

The science behind minimal abandoned carts for marketplace platforms.

Last update

This chapter of the How to create a marketplace guide helps you design your marketplace transaction flow by finding the right approach for matching supply and demand. Also available in audio!

The marketplace transaction flow is complicated, but careful design can make it smooth and secure.

Many early-stage marketplace entrepreneurs pay a lot of attention to how many users sign up for their marketplace. This is a mistake.

User count is a so-called vanity metric—one that doesn't tell you if the marketplace is actually satisfying your users' needs. The purpose of any marketplace is to facilitate transactions between users. Without transactions, your marketplace doesn't provide value to anyone. That's why carefully designing your marketplace transaction process will be time well spent.

In our marketplace glossary, we define a transaction as an exchange of value between a customer and a provider. The transaction may involve money, it may be a barter, or the provider can offer their product or service for free.

One thing you should aim for is high liquidity. By liquidity, we mean the probability of a transaction taking place. This can mean different things for different marketplaces. On Etsy, it means the percentage of products that get sold from all available products. On Airbnb, it means the percentage of rooms that are booked on any given night. On Uber, it means the percentage of drivers out there with a passenger. On Peerby, a request-based marketplace for borrowing things from neighbors, it means the probability of a person being able to borrow a requested item.

Since different types of platforms have vastly different liquidity probabilities, there is no universal liquidity number you should aim for. Nonetheless, it is one of the marketplace metrics you should monitor closely and try to increase as much as possible. High liquidity—in other words, lots of transactions and lots of provided value—should mean happy users.

To reach high liquidity in your marketplace, transactions need to be seamless. In the previous chapter, we covered several ways to help your customers find the product or service they are looking for. However, even if they find what they need, this does not guarantee that a transaction will take place. Many things can still go wrong at that point. In this chapter, we will talk about ways of ensuring the transaction actually ends up happening.

In a nutshell, a marketplace transaction flow can be understood through three steps:

- A customer makes a payment.

- Money is moved to the provider (with the marketplace commission deducted).

- Two-sided reviews.

Seems simple enough, but in reality, marketplace payments are about as complicated as online payment processes get. Let's look at each of these steps in more detail.

The first thing to decide is whether completing the marketplace transaction involves an online payment through your platform or not. Capturing the payment is often essential for your marketplace business model, so the answer is usually yes.

Unfortunately, online payment is also a major source of friction during the transaction, which is why some popular marketplaces like Thumbtack have decided to skip it entirely. The reason is that they want to facilitate a maximum number of transactions and do not want online payment getting in the way. On those sites, the customer and provider simply form an agreement and complete the actual exchange of money outside the platform. Luckily, today there are payment service providers who offer a payment processing solution specifically designed for online marketplace payments and help with making the process as smooth as possible.

If you decide that a payment through your platform is necessary, you will need to select a payment method, define the steps of the checkout process, and choose the point at which the payment occurs.

Credit cards are the most common method of payment since they are used globally. They are especially suitable for online payments since credit card companies usually provide coverage in case of fraud. However, credit cards are not for everyone as they allow people to spend more than they own. For instance, in many countries, it can be tricky for university students to get a credit card. If you are building a tutoring marketplace for university students, this could be a major barrier. Additionally, in certain developing countries, the penetration of credit cards is quite low.

In some countries, paying with a direct bank transfer (or wire transfer) is more popular than paying with a credit card. However, bank transfers are usually not as convenient for marketplaces as they lack features such as fraud protection or the ability to preauthorize payments (more on this later).

After credit cards, PayPal is likely the most well-known global payment method. PayPal is usually available for people who do not have a credit card. With PayPal, it is easy to move money to individuals or companies, even across country borders. PayPal also offers a comprehensive protection program for both buyers and sellers. This is very helpful if the provider is a no-show or if the buyer orders an item and then claims to never have received it. PayPal helps buyers and sellers get their money back in both situations. An additional benefit of using PayPal is trust: many buyers would rather pay with PayPal than share their credit card details with a website they have not heard of before.

Handling online payments is a heavily regulated area. What is more, national regulations regarding online payments may differ and are subject to change. Sometimes, these changes can signify dramatic changes for marketplaces, too. If you don't use existing marketplace software (such as Sharetribe) that provides you with a payment system outside of the box, building your payment system and maintaining its compliance may involve a lot of bureaucracy. If you want your providers to be able to accept credit card payments, you need to either become PCI compliant (which is a very heavy process) or use a marketplace payment gateway that handles the bureaucracy for you. Nowadays, there are many payment service providers focusing on online marketplaces in particular.

PayPal provides such a gateway, so marketplaces using PayPal need not be PCI compliant. Other popular marketplace payment gateways are Stripe Connect, Braintree Marketplace, and MangoPay. There are many differences in how these payment providers handle the payment features that are critical to marketplaces. In addition, there are practical pros and cons to each: Stripe and MangoPay generally charge lower fees than PayPal and are easier to integrate with, but do not have a PayPal-style buyer and seller protection program and are not available in as many countries. In sum: compare payment providers and choose your partner carefully.

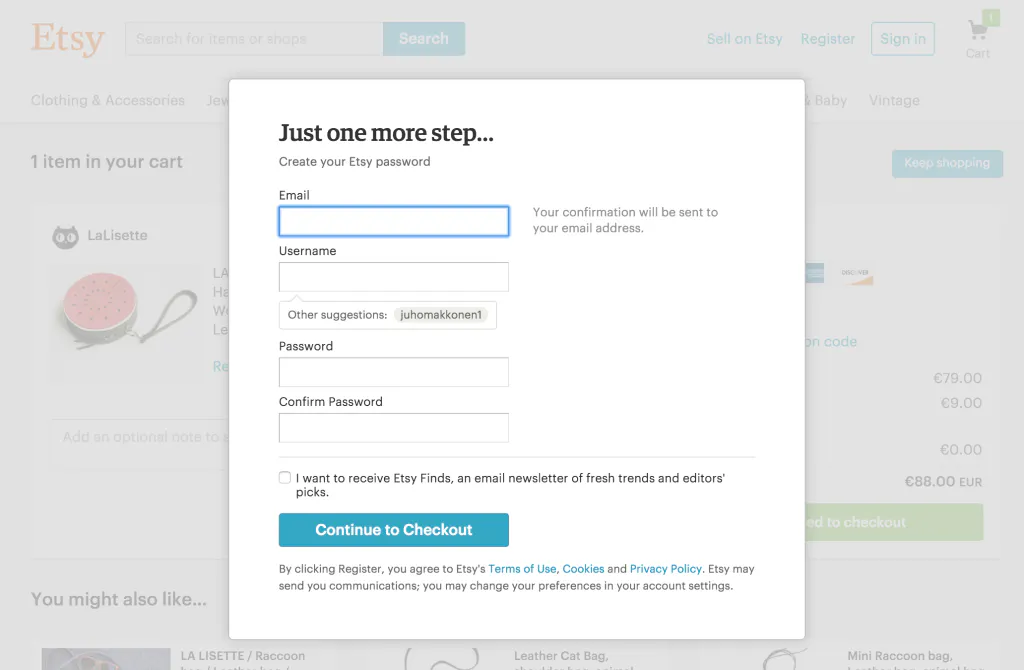

The marketplace checkout process is the set of actions required from the customer to select a product or service, complete the exchange, and (if online payments are used) make the payment. In traditional e-commerce, the most popular checkout experience involves a shopping cart. The customer adds all the desired products to the cart and proceeds to checkout when they are done shopping. If you expect the bulk of your users to make multiple purchases in one session, this is still a great choice.

Many modern marketplaces have noticed that a shopping cart is unnecessary for them. If the marketplace offers rentals, services, or pre-owned products, a shopping cart is far less common. After all, it introduces an extra step: you need to add the product to the cart before being able to proceed to checkout. A good rule of thumb is that you should have as few checkout steps as possible. When using Airbnb, there is no "add to cart" action—when you see something you want, you move to the booking page instantly. In addition, a multi-vendor shopping cart is a complex feature to build, and the costs can easily outweigh the benefits.

A study by Baymard, the e-commerce usability research institute, found that at least 59.8% of potential customers abandon their shopping cart. This clearly shows that it is not enough to get people to start the checkout process. Especially if the process is complicated, people will not follow through. Their large study has lots of detailed information on how to improve the usability of the process. Again, looking at Airbnb, the simplest checkout can be a one-page experience.

An interesting question is whether registration should be mandatory or not during checkout. One would think that skipping the registration or login step is a good idea to make checkout easier. However, most popular marketplaces like Etsy and Airbnb require you to sign up before you can proceed to checkout. They seem to have arrived at the conclusion that the benefit of acquiring a new user outweighs the cost of a potentially lost transaction. Getting more information about users might also be important in preventing fraud and mitigating the risk of other marketplace financial crimes.

On traditional e-commerce sites, the money is transferred immediately after checkout is completed. This process is ideal if the availability and exact price of the product are known beforehand. This is usually the case when you are buying a physical product that is shipped to you.

However, transferring the money immediately does not work as well with rental or service marketplaces. Consider Airbnb. The hosts generally want to review and approve whoever is booking their place before any money exchanges hands. The host may have forgotten to keep their booking calendar up to date, and the place might not be available after all. In some cases, the guest may want to negotiate the final price before paying.

Airbnb offers three different checkout flows. The first one is instant booking, which works just like a traditional e-commerce site: the payment happens without separate approval from the host. This feature needs to be manually enabled by the host.

If the host has not enabled instant booking, the booking can happen in two ways. The first is preauthorization: the guest enters their credit card details and approves the payment, but the money is not transferred. Instead, the credit card company guarantees that the card has enough credit for the money to be transferred during the next seven days. A message is then sent to the host, who can either approve or reject the booking. If they approve it, the credit card is charged. If they reject it, no transfer is made. It should be noted that while preauthorization is possible with credit cards and PayPal, other payment methods (like bank transfers) might not allow it. This is important to keep in mind when choosing your marketplace payment method.

If the guest wants to negotiate the price, they can send a message to the host with a proposal. The host can then pre-approve the price. The guest is notified and prompted to make the payment, after which the money is transferred instantly. Instead of accepting the guest's offer, the host can also reject it or make a pre-approved counteroffer.

These Airbnb-style marketplace transaction flows can also be used in marketplaces that sell physical products. For instance, if the marketplace is used for selling pre-owned wedding dresses that can be tried on before buying, the providers might want to vet customers before letting them into their homes. If a marketplace is used to sell custom-made products, a negotiation between the buyer and seller is often needed before deciding on a final price.

In some service marketplaces, transferring money is even trickier. For example, think of a marketplace for IT freelancers in which work is done by the hour. The customer only knows the hourly price beforehand, and the final price is tallied only after the project is done. Thumbtack often deals with these types of projects, which is likely a major reason why they have not handled online payments so far.

Of course, it is possible to design a platform where the provider can invoice the customer. However, this allows the provider to easily bypass the marketplace payment system by manually sending an invoice. Upwork has addressed the issue by giving providers enough helpful tools to make it worth their while to use the site's billing system.

In an online store, the transaction flow ends once the money is transferred from the customer. Marketplace transaction flows, on the other hand, are more complicated. The money also needs to be transferred to the provider. Despite tremendous advances over the past five years, as of this writing, this process is still surprisingly complicated. There are two main decisions you need to make here: when to move the money to the provider and how to do it.

Your easiest option is to transfer the money directly to the provider once payment is made. There are, however, situations where this might not be the best solution. A big part of your value proposition might be to act as a trusted middleman who guarantees that the customer gets what they ordered. One way to go about this is to delay the provider's payout until the customer confirms receipt of what was ordered.

There are many ways you can handle the relationship between your providers and customers. One is to become a service provider yourself, meaning the transaction essentially happens between you and the customer. This is what Uber does. The drivers are not in a direct financial relationship with the passengers. Uber guarantees the level of service and charges the money. The drivers have a financial relationship with Uber as contractors.

This is a viable approach, but it also means that Uber, as a platform, is responsible for everything that happens in its marketplace, including the level of service. It also opens up another can of worms: it is not obvious whether the providers are really independent contractors or employees. This has resulted in criticism and a class-action lawsuit against Uber. Classifying your providers as employees is a huge financial and regulatory burden. To avoid all of this, it might be better to have the financial relationship be between the customer and the provider.

It is possible to delay the payout without being the service provider yourself. One way is through escrow, where you act as a trusted third party that holds the money for the parties involved. The challenge with this approach is the ensuing legal burden—escrow is a heavily regulated field, and the requirements can vary greatly between countries and regions.

Some payment gateways offer an escrow solution for marketplaces. These solutions reduce the legal burden for the platform owner. Others opt instead to collect credit card details but charge the card only when the money is ready to be moved. This approach creates less regulatory risk but does not guarantee the ability to charge the card when payment is due.

Moving money to your providers sounds like an easy task. Unfortunately, it is not; this is yet another area that is heavily regulated to prevent money laundering.

Before you can move money to an individual, they first need to go through a process called Know Your Customer (KYC) to verify their identity. The type of information depends on the country of the provider and how much money they will be receiving. In general, it is possible to receive up to a few thousand dollars with a lighter review. If the provider expects to receive more money, a heavier process is needed. Stripe has created a comprehensive guide about the required verification information based on your setup. For a complete perspective on global payouts, you can refer to this global payment methods guide put together by payout company Adyen.

The KYC process is likely one reason why marketplaces like OfferUp and Wallapop have decided not to offer an online payment system at all. They want to make it as frictionless as possible for individuals to sell used low-value items, and adding their financial information might be a key barrier that prevents providers from getting started.

From a regulatory perspective, managing multiple countries and currencies in one marketplace can be very tricky. It might be a good idea to start from one country (or just one city)—or at least only have all your providers in the same country—to avoid having to deal with regulatory differences between countries.

If you want to charge a commission for the transaction, you need to decide when and how to charge it. As we discussed above, from a regulatory perspective, receiving all the money and transferring the provider's part to them can be difficult. If you want to avoid this hassle, you should either split the payment into two separate transactions—one goes to the provider and another to you—or move the whole amount to the provider and charge your commission fee from them after the transaction.

After the transaction has taken place, letting the customer and provider review each other is a common tactic. By only allowing ratings after real transactions, you reduce the probability of somebody boosting their reputation by creating dozens of fake reviews. A good reputation is essential for both customers and providers, so having a review system in place works as an incentive to use your payment system and pay your commission. We will go into the details of reputation systems in a chapter dedicated to marketplace trust, but let's quickly go over how to integrate the review system into your transaction flow smoothly.

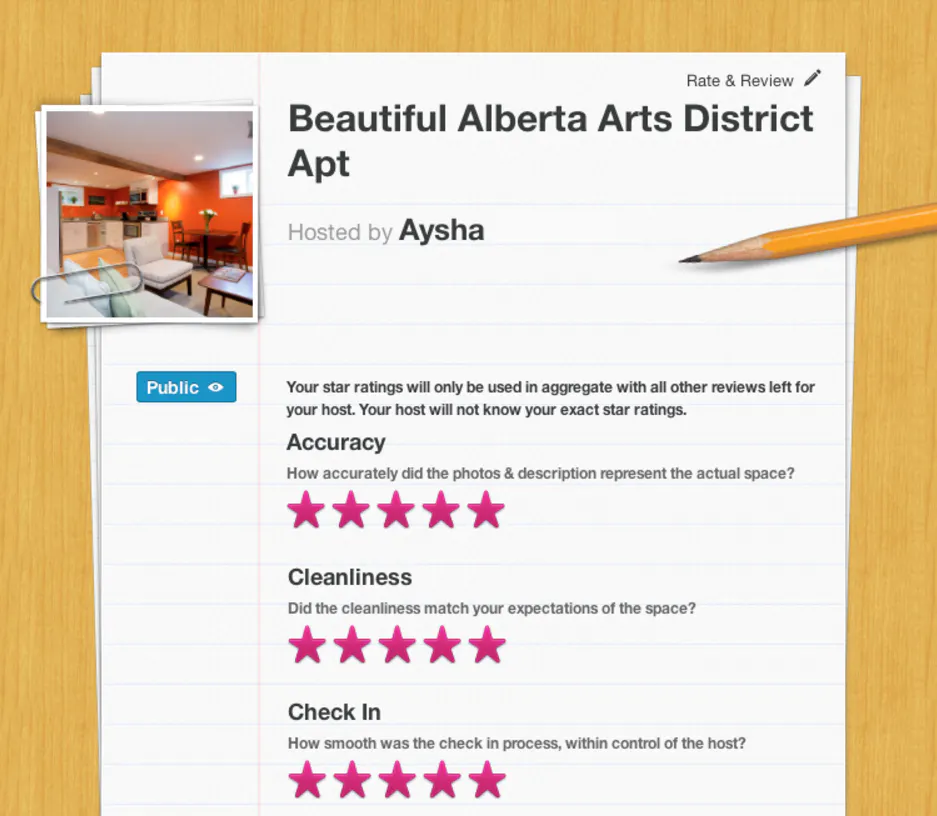

Typically, a review consists of a numeric evaluation (a one to five-star rating, or simple binary thumbs up or down) and a text section. This captures both the quantitative and the qualitative aspects of the review. You might want to ask the parties to give a numeric rating for different aspects of the transaction. This is especially helpful in large marketplaces with lots of providers and reviews—it helps providers differentiate their offerings. For example, Airbnb asks the guest to rate things like communication, cleanliness, and location separately, which all add up to the final rating.

It is important to remember that it only makes sense to leave the review when the actual exchange of products or services has taken place. This means that it (usually) cannot happen right after payment. Your platform needs to know when a transaction has been completed. This can be done automatically (for instance, in the case of rentals, the end date of the rental period), or the customer can be instructed to do it manually (for instance, when they receive the shipped item). Nudging your users by email when it is time to leave the review is a good idea.

When marketplaces grow, the quality of reviews may become an issue. Feedback extortion can be common: "If you're going to give me a bad review, I'll give you one as well". Extortion can also be used to get additional value from the other party. Airbnb tackles extortion cleverly by using a "double-blind" review system: both parties have 14 days to leave the review, after which both reviews are published simultaneously (after either both have left a review or the period is over). Once the reviews are published, they can no longer be altered.

It is now time to put what you have learned into practice and design the marketplace transaction flow for the imaginary marketplace from our previous chapters: a marketplace for personal trainers.

The first decision is whether you want to offer an online payment option or not. As online payment is one of the main value propositions for your trainers, handling payments on your platform is definitely important.

You expect your customers to make repeat purchases through your site and believe reviews are important for the success of your platform. Because of this, you decide to ask customers to log in before they can make a booking. As booking multiple providers at the same time is not a common use case, a shopping cart is not needed. Instead, your customers can book and make a payment directly from the trainer's profile page. You opt for a simple, one-page checkout process that lets customers review all the details at a glance.

Since trainers manage their availability on your site using a calendar, you can allow the customer to make the booking and preauthorize the payment directly without negotiating with the provider. You decide that the providers should be able to choose their customers, so you add a step to let the trainers accept the booking before the money is moved.

You want to avoid the legal burden of escrow, so you decide to preauthorize the credit card when the buyer makes the booking and move the money to the trainer immediately when they accept the booking. To prevent cases of fraud, you choose PayPal as the payment system due to its customer protection program.

Since a big part of your value proposition to customers is an easy way to compare different providers, you include a review system where the customer and the provider can rate each other after the transaction. As your trainers want to know who they are dealing with, you want them to be able to rate their customers—just like the customers rate them. You want to keep things simple in the beginning, so you choose a combination of a star rating and a text description. You decide to send both parties an email notification asking them to leave a review immediately after the first training session has taken place.

This chapter focused on how to make transactions as easy as possible for the users of your platform. There are several steps in a marketplace transaction flow, and decisions need to be made about each one.

The checkout flow should be as simple and have as few steps as possible. The first decision is whether to use online payments or not. The most typical payment methods are credit cards, wire transfers, and PayPal. You should only move the money from the customer when you are sure the transaction will happen.

It can be surprisingly challenging to move money to your providers, mostly due to regulation. If you want to hold money for others, you might need an escrow license. Alternatively, you can become the service provider and make your providers your contractors (or employees) or charge the credit card only after the service has been provided. Your providers will need to go through a verification process before you can move money to them, which can be an issue for marketplaces where individuals trade low-value items.

Reviews are important to build trust in the marketplace. Allow reviews only after monetary transactions to reduce the number of fake reviews. Reviews typically consist of a numeric rating and a text description.

You might also like...

The 5 questions to ask when choosing marketplace software

There are dozens of marketplace software solutions to choose from. These five questions make the right choice for your marketplace idea.

Marketplace payments: The complete guide

Marketplace payments are very complex. This guide helps you list your feature requirements and compare and choose the best marketplace payment provider for you. (Yes, there's a comparison table!)

Your marketplace MVP – How to build a Minimum Viable Platform

What you should focus on when you’re creating the first version of your marketplace platform.

Start your 14-day free trial

Create a marketplace today!

- Launch quickly, without coding

- Extend infinitely

- Scale to any size

No credit card required